E-wallet platforms are built for speed. Users expect to register, verify their identity, transfer funds, and withdraw money within minutes. Fraud networks exploit the same convenience.

Instead of attacking one account at a time, organized groups create and control clusters of accounts. These accounts may be used to abuse promotions, receive stolen funds, test payment instruments, launder scam proceeds, or distribute transactions across multiple identities.

Each registration may appear legitimate. A user may submit a valid identity document, pass facial verification, and complete onboarding. The larger risk becomes visible only when the platform connects device, session, network, behavioral, and transaction signals across accounts.

Why Account-Level Checks Are Not Enough

Traditional fraud controls often assess each account independently. They check whether the identity document is valid, the selfie matches the document portrait, the user passes liveness detection, and the phone number or email address is unique.

These checks remain essential, but they may not detect coordinated abuse.

Fraudsters can use different identities, phone numbers, email addresses, and IP addresses. They may also stagger registrations to avoid velocity rules, making each account appear low risk.

The pattern becomes clearer when multiple accounts share similar device fingerprints, emulator configurations, proxy infrastructure, onboarding behavior, transaction timing, or beneficiary accounts. These connections may indicate that apparently unrelated users are controlled by one operator or fraud group.

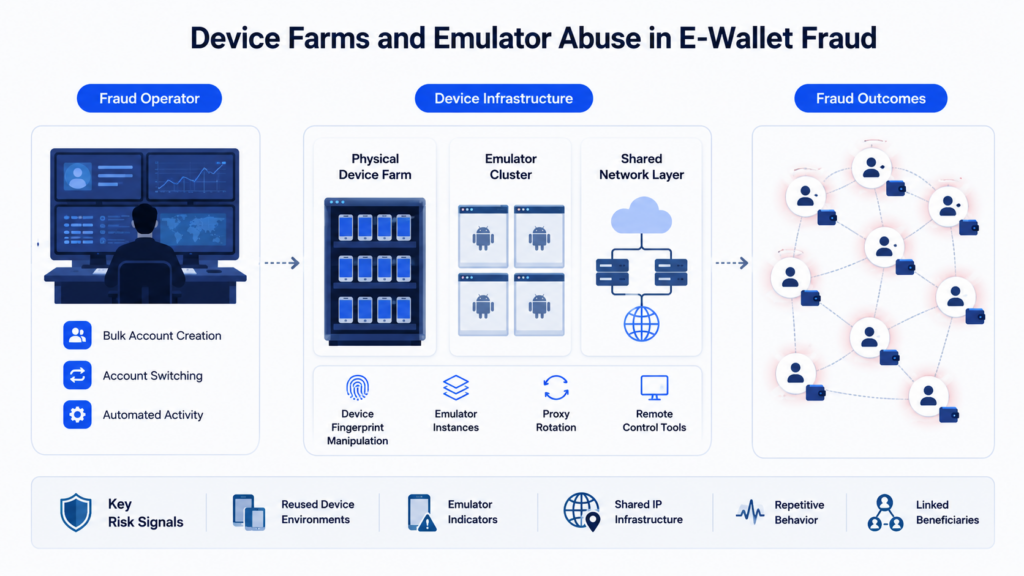

What Are Device Farms and Emulator Abuse?

A device farm operates large numbers of accounts through physical or virtual devices. Some use racks of low-cost smartphones; others rely on Android emulators, cloud devices, virtual machines, or remote-control tools.

Common objectives include promotion abuse, mule account management, payment testing, and evasion of per-device limits.

Emulators make this activity cheaper. A single operator can run multiple virtual mobile devices on one computer or server, with each instance appearing to represent a separate smartphone.

Fraudsters may reset device identifiers, spoof hardware properties, rotate IP addresses, or change application settings. Simple device-ID matching is therefore no longer sufficient. E-wallets need a broader device intelligence layer that evaluates the full technical and behavioral context of each session.

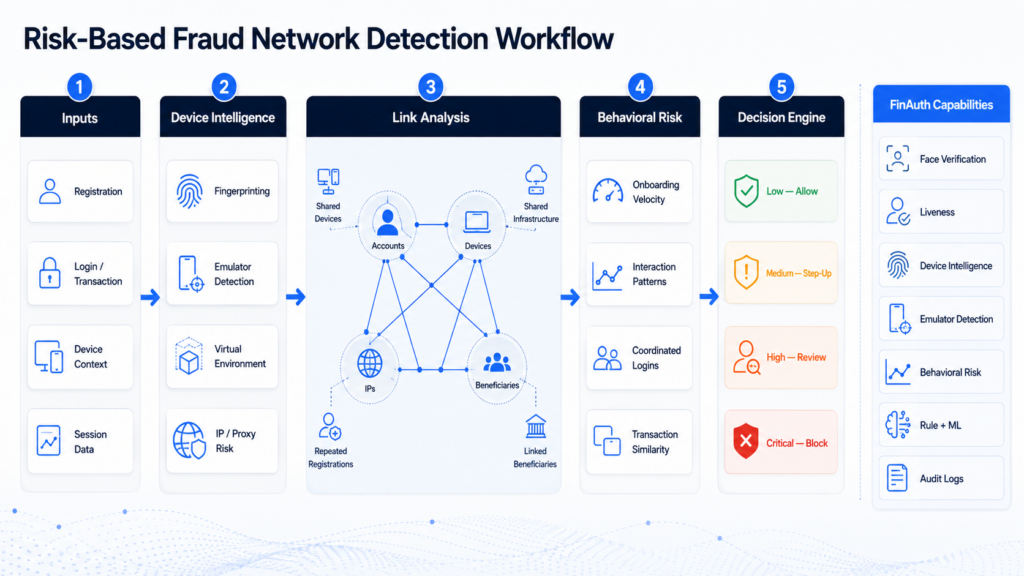

How Device Intelligence Exposes Fraud Networks

Device intelligence analyzes device, application, network, session, and interaction signals to assess risk and identify connections between accounts.

1. Device Fingerprinting

Device fingerprinting creates a persistent profile from attributes such as device model, operating system, screen resolution, language, time zone, hardware characteristics, sensors, and root indicators.

Even when a fraudster resets one identifier, the broader profile may remain similar. If many accounts repeatedly appear from the same environment, the platform can identify a possible multi-account cluster.

2. Emulator and Virtual Environment Detection

Emulator detection evaluates whether the application is running on a genuine consumer device or in a simulated environment.

Possible indicators include virtualized hardware, emulator-specific files, abnormal sensor data, inconsistent device properties, virtual camera usage, modified operating systems, and automation tools.

One emulator signal should not automatically result in a block. However, dozens of accounts sharing emulator characteristics, network infrastructure, and behavioral patterns may justify immediate restriction and investigation.

3. Network and Session Analysis

Fraud networks often rotate IP addresses, but their infrastructure may still reveal common control.

Relevant signals include shared IPs, proxy or VPN use, data-center traffic, geographic inconsistencies, time-zone mismatch, and impossible travel.

A fraud group may use different devices while routing traffic through the same proxy or hosting environment. Combined with device similarity, this creates a stronger link between accounts.

4. Behavioral Analysis

Fraud operators and automation tools often repeat the same actions across accounts.

Signals may include similar onboarding times, repeated interaction patterns, unnaturally fast data entry, identical navigation, coordinated logins, and rapid account switching.

Behavioral analysis is especially valuable when technical identifiers have been hidden or manipulated.

5. Cross-Account Link Analysis

The most important step is connecting signals across the entire e-wallet ecosystem.

Accounts can be represented as nodes in a risk graph. Shared devices, IP addresses, beneficiary accounts, payment instruments, face identities, and session patterns create links between those nodes.

A single shared attribute may be harmless. Multiple overlapping connections can reveal organized abuse.

For example, 30 accounts may use six related emulator fingerprints, connect through three data-center IP ranges, register within short intervals, and transfer funds to the same four beneficiaries. Each account may appear normal in isolation, but the cluster presents a clear network-level risk.

Common E-Wallet Fraud Scenarios

Multi-Account Promotion Abuse

Fraudsters create many accounts to claim welcome rewards, referral bonuses, or cashback. Device intelligence can identify repeated registrations from the same device family, emulator image, or automated environment.

Mule Account Networks

A controller may operate multiple mule accounts used to receive and redistribute scam proceeds. Shared devices, login infrastructure, beneficiary relationships, and transaction timing can expose centralized control.

Stolen Identity Registration

Fraudsters may use legitimate identity documents obtained through leaks, phishing, or social engineering. Even when each identity is different, repeated registrations through the same device farm can indicate industrialized identity misuse.

Account Takeover and Payment Testing

Attackers may access compromised accounts through emulators or remote environments. Sudden changes in device fingerprint, network context, and behavior can trigger step-up verification before funds are transferred. Similar signals can also expose coordinated testing of stolen payment credentials.

Building a Risk-Based Detection Framework

E-wallets should not rely on one signal or a fixed blacklist. Legitimate users may use unusual devices, while fraudsters continuously adapt.

A more effective framework combines identity, device, behavioral, network, and transaction signals.

Low-risk activity can proceed normally when the device is familiar and no suspicious links are found. Medium-risk activity may require additional authentication when a device is new or minor inconsistencies appear. High-risk activity may be restricted when emulator indicators, repeated registrations, abnormal onboarding velocity, or strong cross-account links are present. Critical-risk clusters may be blocked and escalated when many accounts share infrastructure, beneficiaries, and coordinated behavior.

This approach reduces friction for legitimate users while applying stronger controls to organized fraud.

How FinAuth Supports Fraud Network Detection

FinAuth is a next-generation eKYC identity verification platform powered by advanced Large Visual Models.

For e-wallets, FinAuth combines identity verification with device, session, behavioral, and cross-account risk signals to support more complete fraud decisions.

The platform can integrate:

- Document verification and OCR

- Document authenticity analysis

- Face matching

- Edge and cloud liveness detection

- Deepfake and injection attack detection

- Device fingerprinting

- Emulator and virtual environment detection

- Proxy, VPN, and IP risk analysis

- Behavioral risk analysis

- Repeated registration detection

- Rule-based and machine-learning risk decisions

- Full audit logs and evidence retention

An account may pass document and face verification but still be flagged when linked to a suspicious emulator cluster or device farm. Conversely, a legitimate user on a new device may proceed after completing step-up verification.

From Suspicious Accounts to Network-Level Decisions

Fraud networks succeed when platforms evaluate accounts in isolation.

Device intelligence changes the question from “Is this account suspicious?” to “How is this account connected to other devices, sessions, users, and transactions?”

By combining device fingerprinting, emulator detection, behavioral analysis, network intelligence, and cross-account link analysis, e-wallets can identify coordinated abuse earlier, reduce fraud losses, and prevent suspicious funds from moving through the wider payment ecosystem.