Digital lending platforms are designed to make borrowing faster and more accessible. Applicants can complete identity verification remotely, submit documents online, and receive lending decisions without visiting a physical branch.

However, the same streamlined process also creates opportunities for document fraud.

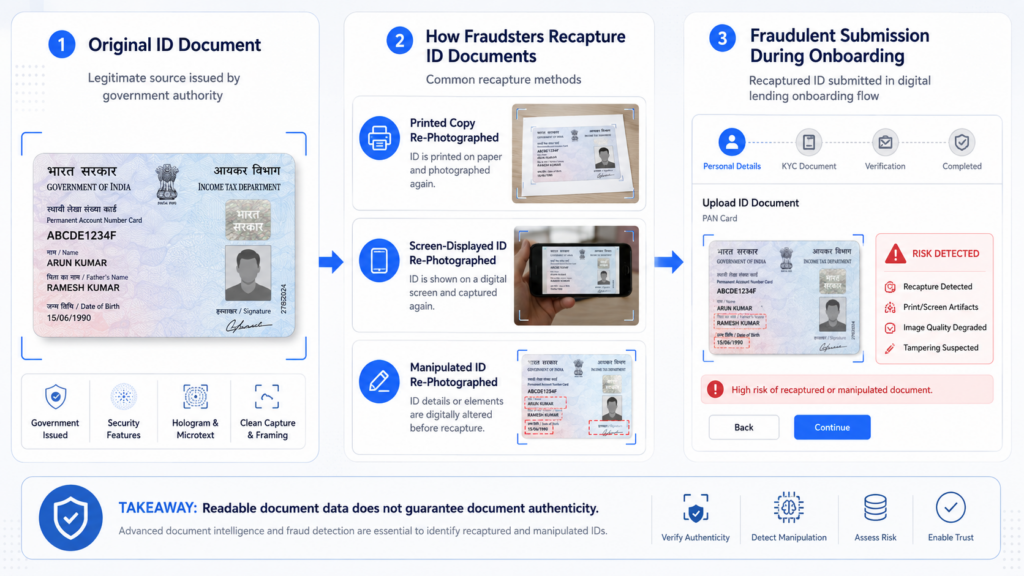

One common example is recaptured ID document fraud. Instead of submitting an original physical identity document, fraudsters upload or photograph a reproduced version, such as a printed copy, a screenshot displayed on another device, or a manipulated image that has been re-photographed to make it appear legitimate.

These documents may still look visually convincing. The name, ID number, portrait, and basic layout can appear correct. Standard OCR tools may even extract the information successfully. But the document itself may not be authentic.

For digital lenders, detecting re-photographed identity documents during onboarding is essential for reducing identity fraud, preventing synthetic identities, and stopping fraudulent loan applications before funds are disbursed.

What Is Recaptured ID Document Fraud?

Recaptured ID document fraud occurs when an applicant submits an image of a reproduced identity document rather than the original document.

The reproduced document may be:

- A photo of a printed copy

- A photo of a photocopied ID

- A screenshot displayed on a phone, tablet, or monitor

- A manipulated document image printed and photographed again

- A digital document edited with image software and shown on another screen

- A photo of an ID image taken from a social media profile, messaging app, or online database

The purpose of recapturing is often to hide visible evidence of image editing or document manipulation.

For example, a fraudster may alter the name, portrait, date of birth, or ID number in a digital image. Instead of uploading the edited file directly, the fraudster displays it on another device or prints it out, then photographs it again. This additional step can remove or obscure some digital traces of manipulation.

As a result, the submitted image may look like a normal camera capture, even though the underlying document is fake.

Why Digital Lending Platforms Are Frequently Targeted

Digital lending platforms often need to balance two competing priorities:

- Providing a fast, frictionless onboarding experience

- Preventing high-risk applicants from exploiting automated approval workflows

Fraudsters understand that lending platforms process large volumes of remote applications and may rely heavily on automated document capture and OCR.

A recaptured document may pass basic checks if the onboarding system only verifies whether:

- Text fields are readable

- The expected document layout is present

- The portrait is visible

- The ID number format is valid

- The required information has been submitted

These checks are necessary, but they are not sufficient.

A document can be readable without being authentic. A fraudulent applicant may submit a high-quality re-photographed image that contains all the expected data fields but does not represent an original identity document.

Common Recaptured Document Scenarios

1. Printed Copies Presented as Original IDs

Fraudsters may print a scanned or manipulated ID document and photograph the printed version during onboarding.

The printed copy can preserve most of the original visual information, including text, portrait images, and document layout. However, it may also introduce subtle inconsistencies in texture, color, edges, and surface reflection.

2. Screen-Based Recapture Attacks

A fraudster may display an identity document image on a phone, laptop, tablet, or monitor and take a new photo of the screen.

Depending on the display quality and camera settings, the submitted image may contain visual signals such as:

- Moiré patterns

- Pixel-grid artifacts

- Screen glare

- Unnatural brightness

- Refresh-line patterns

- Inconsistent color rendering

- Reflections from the surrounding environment

Some high-quality displays make these signals difficult to identify manually, especially when images are reviewed at scale.

3. Edited Documents Re-Photographed to Hide Manipulation

A fraudster may modify an ID image using image-editing tools, then recapture it to reduce visible signs of tampering.

This technique can make traditional image forensics less effective because the uploaded file is no longer the original manipulated image. The system must analyze both the document content and the capture environment.

4. Stolen Identity Documents Reused Across Multiple Applications

In some cases, fraudsters reuse a stolen or leaked ID image across multiple loan applications.

They may display the same image on different devices, crop it differently, change the background, or re-photograph it multiple times. The images may appear slightly different, but the underlying identity asset is the same.

Why OCR Alone Cannot Detect Recaptured Documents

OCR is a critical part of digital onboarding. It extracts structured data from identity documents and helps automate identity verification workflows.

However, OCR primarily answers one question:

Can the system read the document information?

It does not always answer a more important question:

Was the image captured from an authentic physical document?

A re-photographed document can still contain clear and readable text. The OCR engine may accurately extract the name, document number, and date of birth while missing the fact that the image came from a printed copy or digital display.

Effective fraud prevention requires a broader document authenticity assessment.

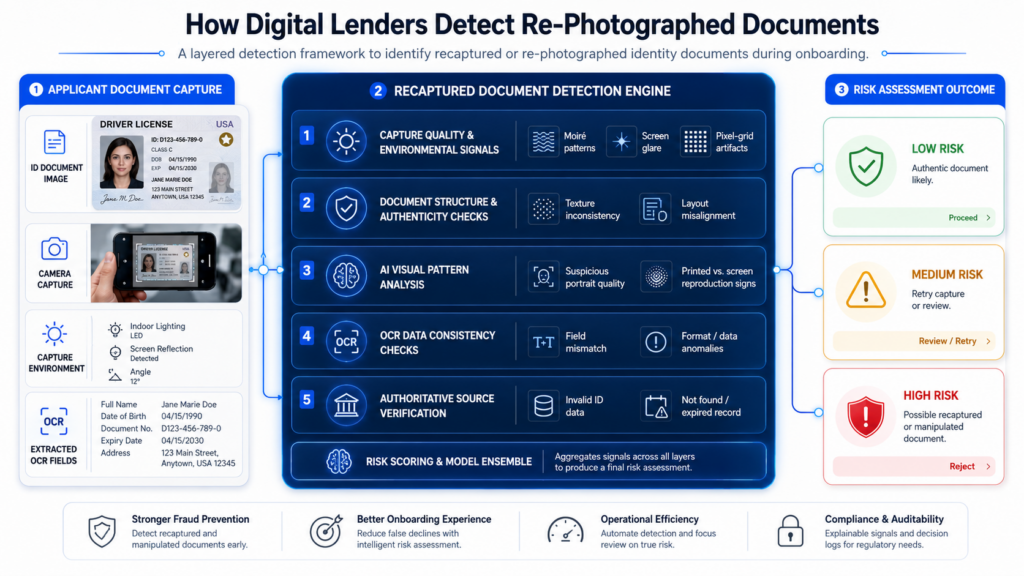

How to Detect Re-Photographed Documents During Onboarding

Digital lenders should combine multiple detection layers rather than rely on a single signal.

1. Analyze Capture Quality and Environmental Signals

The system should inspect how the document image was captured.

Potential indicators of recapture include:

- Screen reflections

- Moiré patterns

- Abnormal surface glare

- Flat or inconsistent texture

- Unnatural document edges

- Irregular shadows

- Display pixels

- Overexposed screen areas

- Background inconsistencies

- Unusual perspective distortion

A single signal may not be enough to classify an image as fraudulent. However, multiple signals can indicate that the applicant is photographing a reproduction rather than an original document.

2. Check Document Structure and Visual Authenticity

Identity documents contain visual patterns that are difficult to reproduce accurately.

A robust document verification system should analyze:

- Document layout

- Portrait placement

- Font consistency

- Text alignment

- Security element positions

- Color distribution

- Background patterns

- Image layering

- Field-level consistency

- Document edges and proportions

This helps identify documents that appear readable but contain structural anomalies.

For example, a manipulated ID may contain a portrait with inconsistent image quality, misaligned text fields, or formatting that does not match the expected template.

3. Use AI Models to Detect Subtle Manipulation Patterns

Rule-based detection can identify obvious anomalies. However, sophisticated recapture attacks often require AI-based visual analysis.

Advanced visual models can evaluate multiple features simultaneously, including texture, lighting, image composition, document geometry, and semantic consistency.

This is especially important when fraudsters use high-resolution screens, professional printers, or image-enhancement tools to create more convincing reproductions.

Instead of checking only whether one specific artifact is present, AI-powered systems can evaluate whether the overall document image behaves like an authentic capture.

4. Validate Extracted Data Against Trusted Sources

Visual checks should be combined with identity data validation where authoritative data sources are available.

For example, lenders can verify whether:

- The ID number is valid

- The document is still active

- The name matches the document number

- The applicant information is consistent with trusted records

- The document has been reported lost, expired, or invalid

Authoritative source verification adds an additional layer of protection. Even when a fraudulent image looks convincing, the underlying identity data may still reveal inconsistencies.

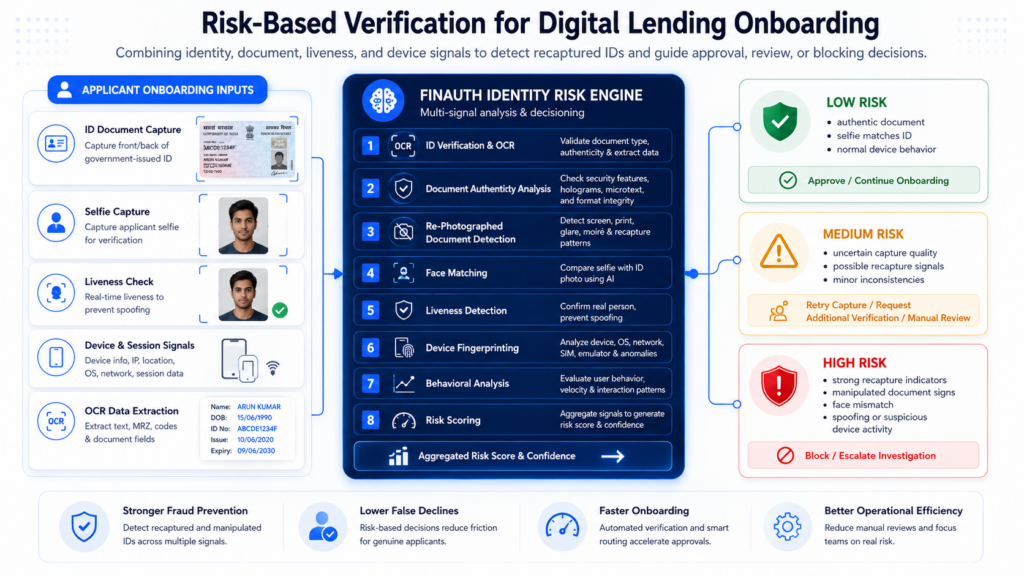

5. Match the ID Portrait Against a Live Selfie

Document verification should not operate in isolation.

After the applicant submits an ID document, the onboarding workflow should compare the ID portrait with a live selfie. This helps confirm whether the person applying for the loan is the legitimate document holder.

A secure workflow should combine:

- ID document verification

- OCR and data extraction

- Document authenticity analysis

- Liveness detection

- Face matching

- Device and behavioral risk signals

This reduces the risk of fraudsters using stolen identity documents or recaptured images belonging to another person.

6. Apply Liveness Detection to Block Presentation and Injection Attacks

Fraudsters may combine a recaptured document with a spoofed selfie, a deepfake video, a replay attack, or an injected image.

Liveness detection helps determine whether the applicant is a real person completing the onboarding session in real time.

Advanced liveness detection should be designed to defend against threats such as:

- Printed photos

- Screen replay attacks

- 3D masks

- Deepfakes

- AIGC-generated faces

- Injection attacks

When document authenticity checks and liveness detection are used together, lenders can identify suspicious applications more effectively.

7. Monitor Device and Session-Level Risk Signals

Fraud is rarely limited to a single manipulated image.

Recaptured document attacks may also be associated with unusual device or behavioral patterns, such as:

- Multiple applications from the same device

- Repeated document uploads

- Abnormal application velocity

- Use of emulators or virtual cameras

- Suspicious IP addresses

- Inconsistent geolocation

- Repeated identity information across different accounts

- Unusual capture behavior

Device fingerprinting and behavioral analysis can help lenders identify coordinated fraud attempts that may not be obvious from document analysis alone.

A Risk-Based Verification Workflow for Digital Lending

A practical onboarding workflow can apply different actions depending on the detected risk level.

Low-Risk Applications

When the document appears authentic, the selfie matches the ID portrait, and no unusual device signals are detected, the user can continue through the standard onboarding process.

Medium-Risk Applications

When the system identifies uncertain document quality, possible recapture indicators, or minor inconsistencies, the lender can request:

- A new document capture

- A different capture angle

- An additional selfie

- More identity information

- Manual review

High-Risk Applications

When the system detects strong evidence of screen recapture, manipulated document content, face mismatch, spoofing attempts, or repeated suspicious activity, the application should be blocked or escalated for further investigation.

This risk-based approach helps lenders improve fraud prevention without adding unnecessary friction for legitimate users.

How FinAuth Helps Detect Identity Fraud During Digital Lending Onboarding

FinAuth is a next-generation eKYC identity verification platform powered by advanced Large Visual Models (LVM).

For digital lending platforms, FinAuth helps create a more secure onboarding workflow by combining multiple identity verification capabilities in one integrated process.

Global ID Verification and OCR

FinAuth supports more than 10,000 identity document types across over 200 countries, enabling automated document data extraction and identity verification for international lending scenarios.

Document Authenticity Assessment

FinAuth helps identify suspicious identity document submissions by analyzing visual inconsistencies, document structure, and capture-related risk signals.

This helps lenders detect cases where applicants submit printed copies, screen-displayed images, manipulated documents, or other reproduced identity assets.

Authoritative Source Verification

Where supported, FinAuth can validate identity data against authoritative sources, adding another layer of protection beyond visual document checks.

Liveness Detection and Face Matching

FinAuth combines LVM-powered multimodal liveness detection with millisecond-level 1:1 face matching to verify that the person completing the application is the legitimate ID document holder.

The system is designed to defend against advanced threats such as 3D masks, deepfakes, AIGC content, and injection attacks.

Device Fingerprinting and Behavioral Analysis

FinAuth also incorporates device fingerprinting and behavioral analysis to identify suspicious onboarding patterns and coordinated fraud attempts.

Conclusion

Recaptured ID document fraud is more than a document-quality issue. It is an identity risk problem.

A printed copy, screen-displayed image, or re-photographed manipulated ID may still contain readable text and recognizable document elements. Basic OCR checks alone may not be enough to detect the fraud.

Digital lending platforms need a layered approach that combines document authenticity analysis, AI-powered visual inspection, authoritative source verification, liveness detection, face matching, and device-level risk assessment.

By detecting re-photographed documents during onboarding, lenders can stop suspicious applications earlier, reduce fraud losses, and build a more secure digital lending experience.